Peter O’Neill, the former prime minister of Papua New Guinea, was at the epicentre of the controversial $1.3 billion UBS loan that was the subject of a royal commission. But on Thursday he joined his political foe, current prime minister James Marape, in calling on the Australian branch of the Swiss bank to repay the Pacific Island nation. Ex-PNG prime minister Peter O’Neill was heavily criticised at the inquiry. AP

The collar loan: The story behind UBS’ ill-fated Papua New Guinea deal

by Jonathan Shapiro and Lisa Murray | FINANCIAL REVIEW , Apr 21, 2022 – 8.05pm.

Peter O’Neill, the former prime minister of Papua New Guinea, was at the epicentre of the controversial $1.3 billion UBS loan that was the subject of a royal commission.

But on Thursday he joined his political foe, current prime minister James Marape, in calling on the Australian branch of the Swiss bank to repay the Pacific Island nation.

Ex-PNG prime minister Peter O’Neill was heavily criticised at the inquiry. AP

“The advice received by myself and the state from UBS and financial advisers with serious conflicts were not done in the best interests of the state,” O’Neill proclaimed in a statement the day after the weighty 576-page report was handed out in parliament.

That royal commission called for O’Neill to face a corruption inquiry and prosecution for providing false statements.

It was a fate he said he was willing to accept, but as he prepared to fight for power in the coming general election he pledged to pursue his willing financiers.

“These professionals, including UBS, have provided misleading advice to government and any government coming in after elections must pursue recovery of the monies paid,” O’Neill claimed.

The comments will not be welcomed at UBS’s Sydney headquarters in Chifley Tower.

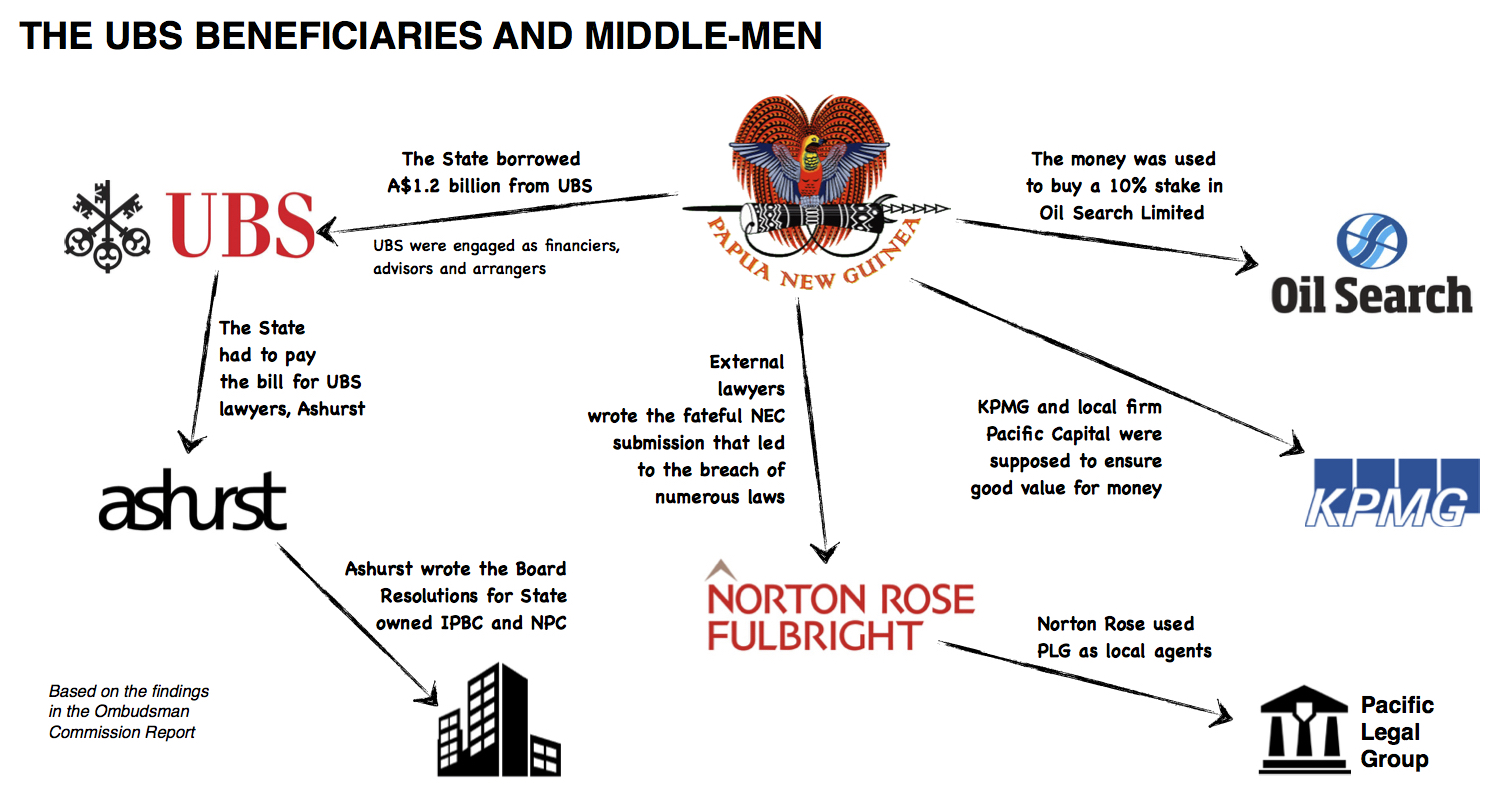

More than eight years ago, in March 2014, those walls were celebrating the lucrative and complex $1.3 billion loan to PNG. Months later the bonuses flowed to the Port Moresby deal-makers and derivative number-crunchers that met the tight deadline.

But it’s a deal that won’t go away even if many of the staffers involved have moved on. While the bank netted around $100 million in fees and revenues from its role in financing PNG, the state lost an estimated $340 million dollars.

Advertisement

The disastrous outcome for PNG has led MPs in the Pacific Island nation to stop at nothing to hold their political foes accountable while seeking vengeance for an opportunity forever lost.

And that is why on Wednesday, as a power outage sent PNG’s Peoples House into darkness, thick stacks of white paper – the findings of the two and a half year royal commission into the loan – were symbolically handed out to the nation’s members of parliament.

This was a royal commission aided by some of Australia’s brightest legal minds that cost the nation $11 million. No one, including the prime minister, could escape its reach.

With an election looming, its findings will no doubt be politicised further. But MPs are determined to look beyond PNG and the reach of the commission for restitution.

UBS, the commission said, should pay back $175 million it was calculated to have overcharged while local and Australian regulators should be approached to pursue civil or criminal charges. The bank and some of its staff should also be banned for failing to cooperate with the commission.

UBS breaks silence

But the bank, which had remained silent until the report was finalised, is adamant it acted appropriately and transparently.

It was scathing of the commission’s findings and says its side simply wasn’t heard. It took particular exception to the findings of US experts, hired to unpick the complex transactions.

So, what did UBS do to incur the wrath of the commission, and is it warranted?

Is the investment bank a convenient scapegoat or did it transfer wealth from PNG through conflict and complexity as the commission alleges?

To answer this, we need to understand why the deal was done in the first place.

The genesis of that is in the vast natural resources of PNG, in particular its abundance of liquefied natural gas.

The $US19 billion PNG LNG project was the nation’s most significant undertaking and while multinational oil companies and global financiers would provide the expertise and capital, the sovereign had the rights to acquire 19.4 per cent of the lucrative project.

However, PNG was required to front the funds at a most inopportune time – in 2009 when global capital markets were all but shut to developing nation borrowers.

So the nation’s leaders came up with a plan. They agreed to effectively pledge the long-held ownership stake in national champion oil firm Oil Search to the United Arab Emirates sovereign wealth fund IPIC in the form of a $1.7 billion exchangeable bond.

James Marape discusses the royal commission report into UBS loan on Wednesday.

The borrowings would pay for its share of PNG LNG that would prove invaluable in amassing its sovereign wealth. By offering IPIC the rights to buy its stake in Oil Search, the interest rate on the loan was toggled to a more affordable rate of 5.1 per cent.

But it meant that by March 2014, IPIC could take up the option to buy PNG out of Oil Search, which it duly did.

As that date approached, Oil Search and PNG fretted about the pending outcome with the latter seeking input from Sydney’s investment banks.

Oil Search, meanwhile, was considering buying into another PNG development in the Elk Antelope gas field.

A consortium controlled by Swiss businessman Carlo Civelli, via Canadian company Interoil and private company PAC LNG, held the rights to the field. In early 2014 French oil giant Total had bought a 60 per cent stake in Elk Antelope and Oil Search was itself racing to get in on the action.

A proposal was tabled whereby Oil Search would issue more shares, equivalent to 10 per cent of its register, that PNG would take up via a placement. The proceeds would allow Oil Search to buy 23 per cent of the project and restore PNG’s ownership in its national champion corporation.

To pay for those shares PNG needed to once again borrow money. UBS won the beauty parade and proposed a collar loan solution to keep costs down.

The bank hastily arranged the relevant documents as time was of the essence for Oil Search. Such an important transaction would also require approval from PNG’s executive council.

But few in government including Treasurer Don Poyle were aware of the hastily arranged loan transaction that may have breached the state’s debt ratios were it not shifted to a state-owned enterprise called Kumul Petroleum.

Polye was sacked after refusing to sign off on the loan because of concerns about its impact on the budget. That ensured the loan was treated with suspicion from its very inception.

Deal not necessary

Why PNG felt they needed to buy back into Oil Search is a matter of contention.

The royal commission determined that the entire ill-fated deal was not necessary and that the state could simply have waited until it was entitled to invest directly in the Elk Antelope project as it had with the PNG LNG project.

The alleged ties between senior officials and Civelli, who the commission said was the benefactor of the proceeds from the transaction, has long since been a matter of speculation.

In parliament on Wednesday prime minister Marape didn’t mince his words as he made direct reference to the Swiss businessman who he said often dines with the nation’s political class in the country’s capital.

“All roads lead you to Mr Civelli, all roads lead to you Oil Search and all roads lead to UBS,” Marape claimed on Wednesday as the heavy stacks of the royal commission were handed to a packed floor.

“And sadly all roads lead to you, Member for Ialibu-Pangia,” he suggested in a reference to the former prime minister and political foe O’Neill, who he toppled in part due to the controversy of the UBS loan.

O’Neill, the report recommended, should face the anti-corruption inquiry, which he said he was prepared to do as he alleged Marape had politicised the expensive commission.

Where Marape and his political foe seemed to agree on was that UBS should be pursued for its role.

But what in fact did UBS do or not do?

First the loan was structured in two parts, a $335 million bridging loan and a $905 million two-year collar loan.

The former is a loan that can be repaid but interest rates step up if the borrower cannot do so. The collar loan is more complicated and involves the use of options derivatives.

“The essence of the loan is that it is generally structured so that the lender has no risk of default by the borrower,” the counsel assisting’s final submission said.

“This is done by ensuring that all of the interest is paid at the outset of the loan, having the shares as collateral and using options.”

A collar loan is fairly common. It allows the borrower, in this case UBS, to take security of shares, in this case PNG’s newly acquired Oil Search shares, and use option contracts to protect its position.

So, even if the Oil Search price fell, the put options (which give the holder the right to sell shares at an agreed price) would gain in value and allow the total loan amount to be repaid.

And that is exactly what happened. After four years of stable energy prices, a supply glut overwhelmed demand. The price of a barrel of oil fell from above $US100 in June 2014 to around $US50. Oil Search shares got hit and the PNG government was nursing a loss on its shares.

PNG refinanced its collar loan twice in December 2014 and February 2016. But eventually in September 2017 the collar loan was unwound through the sale of Oil Search shares at $6.20 – a loss of $224 million.

The position of UBS, which netted about $100 million in fees and revenues associated with the transaction, was protected.

Brattle battle

But how much did the state lose on this transaction after all the fees and opportunity cost associated with the transaction? That is the heart of tensions between the royal commission, which has called for UBS to repay a $175 million amount they say the state was overcharged, by the Swiss bank.

The commission alleges UBS misled PNG in claiming the options written in the collar loan were priced at cost, and was conflicted in providing both advice and financing PNG in the ill-fated loan.

This is the basis for its call that civil or criminal penalties should be sought.

The commission arrived at this conclusion for two reasons.

One is that it claims UBS did not cooperate fully with the commission. While documents were provided, the Australian branch, according to the commission, did not provide any witnesses that could be cross-examined to determine the contents of the documents it provided, or to ascertain what truly occurred.

UBS, on the other hand, says it assisted the commission and challenged adverse findings and that the state’s only losses were as a result of the Oil Search share price decline, which had nothing to do with it.

Privately officials within the bank who are dealing with the fallout are frustrated by the fact that most of the senior operatives involved in the transaction are no longer at UBS and could not be compelled, given they’re in Australia, to front the commission.

That would no doubt include the senior ranks of the bank at the time, Matthew Grounds and Guy Fowler, who in March 2020 decamped to create a rival investment bank Barrenjoey, among others.

The revolving-doors nature of Australian investment banking was not lost on Marape as he addressed parliament.

“All the UBS executives that facilitated the transaction retired from office,” he said.

“But let me remind UBS … or any international company for that matter. PNG is not what we were in 1975 [when the nation was formed]. We are much better than last time.”

That’s of little consolation to UBS’ current leadership ranks, or of little concern to the commission that has called for a ten-year ban for the bank, and a five-year ban for two senior staffers still at UBS, Patrick Jilek and Mitch Turner.

Then there is the $175 million amount which UBS is alleged to have overcharged.

The commission hired United States-based consultancy Brattle Group to work through the terms of the deal to assess whether PNG got a fair deal from UBS.

Dr George Oldfield, a derivatives expert at Brattle who previously worked at the US Securities and Exchange Commission and the Federal Reserve, testified at the commission and described the transactions as “not fairly priced” and “unnecessarily complicated”.

The apparently unfair interest rate above the risk-free rate amounted to $88.4 million of the calculated amount that was over-charged.

UBS vehemently disagreed that a risk-free rate should be applied given it could not borrow at that amount and took most of Brattle’s calculations to task.

The balance of the overcharged amount was the difference between what Brattle calculated to be a fair price of the options contracts used in the collar loan the price PNG was actually charged.

Again UBS contends that the models used by Brattle and its inputs were flawed, which undermines the overcharged amount.

UBS did detail that it made a revenue of $48.6 million in relation to the collar loans and says the commission made no attempt to reconcile this amount with its $175 million figure.

That itself leads to another point of contention. The commission has said UBS may have engaged in misleading and deceptive conduct by representing to PNG that the options used in the collar loan were written at nil-premium.

“That is, nil premium in this context was a clear representation by UBS that it was not separately profiting from the pricing of the option structure over and above its declared fees,” is what the commissioner assisting determined it meant, which was at odds with the work of Brattle.

UBS had, in fact, set the pricing to make money and says it never suggested otherwise.

It claims it did not misrepresent the state through its nil premium claim, and cited contract protocols that this definition applied to a payment due at a certain date. Given all the interest had been paid upfront, the nil premium description was appropriate, UBS said.

On that, the commission said UBS knew that PNG wanted to borrow money at a rate below 5 per cent, so it could be compared favourably with the 5.1 per cent IPIC loan.

The two-year collar loan was represented at a 4.95 per cent rate, but the commission said that since PNG effectively paid at the outset of the loan the implied rate was 5.34 per cent. While that is the case, other terms of the loan may have adjusted.

So UBS has indeed mounted a vigorous and spirited defence against a commission it says has not heard it and relied on flawed evidence.

UBS needs to disclose how much it earned as part of the Oil Search deal.

Time for UBS to come clean on PNG loan

But the commission’s comments show that it is steadfast in its view that the bank left it too late and that its expert is both credible and correct. By failing to produce any witnesses it ceded its opportunity to set the record straight.

Whether this will have implications for UBS beyond a week of bad headlines also remains to be seen.

A new PNG government can’t reverse a deal their formers leaders pursued but have now been told should never have been done, by any bank.

But those very leaders seem to agree that UBS, which itself is under new leadership, should be pursued. That means the consequences of the ill-fated deal will linger uncomfortable in Chifley Tower for a while yet.

The collar loan: The story behind UBS’ ill-fated PNG deal.

Read more news and stories here. Watch online news and documentaries about Papua New Guinea here.

Opposition Leader James Nomane criticises the PNG government over economic damage affecting young graduates and calls for a Vote of No Confidence to restore leadership.

PNG Opposition Leader and Member for Chuave Hon, James Nomane urges graduates to stop waiting for opportunities and instead “build their own door,” highlighting unemployment, corruption, and the need for discipline and leadership among young people

Many Papua New Guineans know Anslom Nakikus as a famous reggae singer. But fewer people know that he is also a well-educated man who studied at the University of Papua New Guinea and the University of Goroka before rising to international music success. His story shows how education and talent can work together to inspire a generation.

Deal not necessary

Why PNG felt they needed to buy back into Oil Search is a matter of contention.

The royal commission determined that the entire ill-fated deal was not necessary and that the state could simply have waited until it was entitled to invest directly in the Elk Antelope project as it had with the PNG LNG project.

The alleged ties between senior officials and Civelli, who the commission said was the benefactor of the proceeds from the transaction, has long since been a matter of speculation.

In parliament on Wednesday prime minister Marape didn’t mince his words as he made direct reference to the Swiss businessman who he said often dines with the nation’s political class in the country’s capital.

“All roads lead you to Mr Civelli, all roads lead to you Oil Search and all roads lead to UBS,” Marape claimed on Wednesday as the heavy stacks of the royal commission were handed to a packed floor.

“And sadly all roads lead to you, Member for Ialibu-Pangia,” he suggested in a reference to the former prime minister and political foe O’Neill, who he toppled in part due to the controversy of the UBS loan.

O’Neill, the report recommended, should face the anti-corruption inquiry, which he said he was prepared to do as he alleged Marape had politicised the expensive commission.

Where Marape and his political foe seemed to agree on was that UBS should be pursued for its role.

But what in fact did UBS do or not do?

First the loan was structured in two parts, a $335 million bridging loan and a $905 million two-year collar loan.

The former is a loan that can be repaid but interest rates step up if the borrower cannot do so. The collar loan is more complicated and involves the use of options derivatives.

“The essence of the loan is that it is generally structured so that the lender has no risk of default by the borrower,” the counsel assisting’s final submission said.

“This is done by ensuring that all of the interest is paid at the outset of the loan, having the shares as collateral and using options.”

A collar loan is fairly common. It allows the borrower, in this case UBS, to take security of shares, in this case PNG’s newly acquired Oil Search shares, and use option contracts to protect its position.

So, even if the Oil Search price fell, the put options (which give the holder the right to sell shares at an agreed price) would gain in value and allow the total loan amount to be repaid.

And that is exactly what happened. After four years of stable energy prices, a supply glut overwhelmed demand. The price of a barrel of oil fell from above $US100 in June 2014 to around $US50. Oil Search shares got hit and the PNG government was nursing a loss on its shares.

PNG refinanced its collar loan twice in December 2014 and February 2016. But eventually in September 2017 the collar loan was unwound through the sale of Oil Search shares at $6.20 – a loss of $224 million.

The position of UBS, which netted about $100 million in fees and revenues associated with the transaction, was protected.

Brattle battle

But how much did the state lose on this transaction after all the fees and opportunity cost associated with the transaction? That is the heart of tensions between the royal commission, which has called for UBS to repay a $175 million amount they say the state was overcharged, by the Swiss bank.

The commission alleges UBS misled PNG in claiming the options written in the collar loan were priced at cost, and was conflicted in providing both advice and financing PNG in the ill-fated loan.

This is the basis for its call that civil or criminal penalties should be sought.

The commission arrived at this conclusion for two reasons.

One is that it claims UBS did not cooperate fully with the commission. While documents were provided, the Australian branch, according to the commission, did not provide any witnesses that could be cross-examined to determine the contents of the documents it provided, or to ascertain what truly occurred.

UBS, on the other hand, says it assisted the commission and challenged adverse findings and that the state’s only losses were as a result of the Oil Search share price decline, which had nothing to do with it.

Privately officials within the bank who are dealing with the fallout are frustrated by the fact that most of the senior operatives involved in the transaction are no longer at UBS and could not be compelled, given they’re in Australia, to front the commission.

That would no doubt include the senior ranks of the bank at the time, Matthew Grounds and Guy Fowler, who in March 2020 decamped to create a rival investment bank Barrenjoey, among others.

The revolving-doors nature of Australian investment banking was not lost on Marape as he addressed parliament.

“All the UBS executives that facilitated the transaction retired from office,” he said.

“But let me remind UBS … or any international company for that matter. PNG is not what we were in 1975 [when the nation was formed]. We are much better than last time.”

That’s of little consolation to UBS’ current leadership ranks, or of little concern to the commission that has called for a ten-year ban for the bank, and a five-year ban for two senior staffers still at UBS, Patrick Jilek and Mitch Turner.

Then there is the $175 million amount which UBS is alleged to have overcharged.

The commission hired United States-based consultancy Brattle Group to work through the terms of the deal to assess whether PNG got a fair deal from UBS.

Dr George Oldfield, a derivatives expert at Brattle who previously worked at the US Securities and Exchange Commission and the Federal Reserve, testified at the commission and described the transactions as “not fairly priced” and “unnecessarily complicated”.

The apparently unfair interest rate above the risk-free rate amounted to $88.4 million of the calculated amount that was over-charged.

UBS vehemently disagreed that a risk-free rate should be applied given it could not borrow at that amount and took most of Brattle’s calculations to task.

The balance of the overcharged amount was the difference between what Brattle calculated to be a fair price of the options contracts used in the collar loan the price PNG was actually charged.

Again UBS contends that the models used by Brattle and its inputs were flawed, which undermines the overcharged amount.

UBS did detail that it made a revenue of $48.6 million in relation to the collar loans and says the commission made no attempt to reconcile this amount with its $175 million figure.

That itself leads to another point of contention. The commission has said UBS may have engaged in misleading and deceptive conduct by representing to PNG that the options used in the collar loan were written at nil-premium.

“That is, nil premium in this context was a clear representation by UBS that it was not separately profiting from the pricing of the option structure over and above its declared fees,” is what the commissioner assisting determined it meant, which was at odds with the work of Brattle.

UBS had, in fact, set the pricing to make money and says it never suggested otherwise.

It claims it did not misrepresent the state through its nil premium claim, and cited contract protocols that this definition applied to a payment due at a certain date. Given all the interest had been paid upfront, the nil premium description was appropriate, UBS said.

On that, the commission said UBS knew that PNG wanted to borrow money at a rate below 5 per cent, so it could be compared favourably with the 5.1 per cent IPIC loan.

The two-year collar loan was represented at a 4.95 per cent rate, but the commission said that since PNG effectively paid at the outset of the loan the implied rate was 5.34 per cent. While that is the case, other terms of the loan may have adjusted.

So UBS has indeed mounted a vigorous and spirited defence against a commission it says has not heard it and relied on flawed evidence.

UBS needs to disclose how much it earned as part of the Oil Search deal.

Time for UBS to come clean on PNG loan

But the commission’s comments show that it is steadfast in its view that the bank left it too late and that its expert is both credible and correct. By failing to produce any witnesses it ceded its opportunity to set the record straight.

Whether this will have implications for UBS beyond a week of bad headlines also remains to be seen.

A new PNG government can’t reverse a deal their formers leaders pursued but have now been told should never have been done, by any bank.

But those very leaders seem to agree that UBS, which itself is under new leadership, should be pursued. That means the consequences of the ill-fated deal will linger uncomfortable in Chifley Tower for a while yet.

The collar loan: The story behind UBS’ ill-fated PNG deal.

Deal not necessary

Why PNG felt they needed to buy back into Oil Search is a matter of contention.

The royal commission determined that the entire ill-fated deal was not necessary and that the state could simply have waited until it was entitled to invest directly in the Elk Antelope project as it had with the PNG LNG project.

The alleged ties between senior officials and Civelli, who the commission said was the benefactor of the proceeds from the transaction, has long since been a matter of speculation.

In parliament on Wednesday prime minister Marape didn’t mince his words as he made direct reference to the Swiss businessman who he said often dines with the nation’s political class in the country’s capital.

“All roads lead you to Mr Civelli, all roads lead to you Oil Search and all roads lead to UBS,” Marape claimed on Wednesday as the heavy stacks of the royal commission were handed to a packed floor.

“And sadly all roads lead to you, Member for Ialibu-Pangia,” he suggested in a reference to the former prime minister and political foe O’Neill, who he toppled in part due to the controversy of the UBS loan.

O’Neill, the report recommended, should face the anti-corruption inquiry, which he said he was prepared to do as he alleged Marape had politicised the expensive commission.

Where Marape and his political foe seemed to agree on was that UBS should be pursued for its role.

But what in fact did UBS do or not do?

First the loan was structured in two parts, a $335 million bridging loan and a $905 million two-year collar loan.

The former is a loan that can be repaid but interest rates step up if the borrower cannot do so. The collar loan is more complicated and involves the use of options derivatives.

“The essence of the loan is that it is generally structured so that the lender has no risk of default by the borrower,” the counsel assisting’s final submission said.

“This is done by ensuring that all of the interest is paid at the outset of the loan, having the shares as collateral and using options.”

A collar loan is fairly common. It allows the borrower, in this case UBS, to take security of shares, in this case PNG’s newly acquired Oil Search shares, and use option contracts to protect its position.

So, even if the Oil Search price fell, the put options (which give the holder the right to sell shares at an agreed price) would gain in value and allow the total loan amount to be repaid.

And that is exactly what happened. After four years of stable energy prices, a supply glut overwhelmed demand. The price of a barrel of oil fell from above $US100 in June 2014 to around $US50. Oil Search shares got hit and the PNG government was nursing a loss on its shares.

PNG refinanced its collar loan twice in December 2014 and February 2016. But eventually in September 2017 the collar loan was unwound through the sale of Oil Search shares at $6.20 – a loss of $224 million.

The position of UBS, which netted about $100 million in fees and revenues associated with the transaction, was protected.

Brattle battle

But how much did the state lose on this transaction after all the fees and opportunity cost associated with the transaction? That is the heart of tensions between the royal commission, which has called for UBS to repay a $175 million amount they say the state was overcharged, by the Swiss bank.

The commission alleges UBS misled PNG in claiming the options written in the collar loan were priced at cost, and was conflicted in providing both advice and financing PNG in the ill-fated loan.

This is the basis for its call that civil or criminal penalties should be sought.

The commission arrived at this conclusion for two reasons.

One is that it claims UBS did not cooperate fully with the commission. While documents were provided, the Australian branch, according to the commission, did not provide any witnesses that could be cross-examined to determine the contents of the documents it provided, or to ascertain what truly occurred.

UBS, on the other hand, says it assisted the commission and challenged adverse findings and that the state’s only losses were as a result of the Oil Search share price decline, which had nothing to do with it.

Privately officials within the bank who are dealing with the fallout are frustrated by the fact that most of the senior operatives involved in the transaction are no longer at UBS and could not be compelled, given they’re in Australia, to front the commission.

That would no doubt include the senior ranks of the bank at the time, Matthew Grounds and Guy Fowler, who in March 2020 decamped to create a rival investment bank Barrenjoey, among others.

The revolving-doors nature of Australian investment banking was not lost on Marape as he addressed parliament.

“All the UBS executives that facilitated the transaction retired from office,” he said.

“But let me remind UBS … or any international company for that matter. PNG is not what we were in 1975 [when the nation was formed]. We are much better than last time.”

That’s of little consolation to UBS’ current leadership ranks, or of little concern to the commission that has called for a ten-year ban for the bank, and a five-year ban for two senior staffers still at UBS, Patrick Jilek and Mitch Turner.

Then there is the $175 million amount which UBS is alleged to have overcharged.

The commission hired United States-based consultancy Brattle Group to work through the terms of the deal to assess whether PNG got a fair deal from UBS.

Dr George Oldfield, a derivatives expert at Brattle who previously worked at the US Securities and Exchange Commission and the Federal Reserve, testified at the commission and described the transactions as “not fairly priced” and “unnecessarily complicated”.

The apparently unfair interest rate above the risk-free rate amounted to $88.4 million of the calculated amount that was over-charged.

UBS vehemently disagreed that a risk-free rate should be applied given it could not borrow at that amount and took most of Brattle’s calculations to task.

The balance of the overcharged amount was the difference between what Brattle calculated to be a fair price of the options contracts used in the collar loan the price PNG was actually charged.

Again UBS contends that the models used by Brattle and its inputs were flawed, which undermines the overcharged amount.

UBS did detail that it made a revenue of $48.6 million in relation to the collar loans and says the commission made no attempt to reconcile this amount with its $175 million figure.

That itself leads to another point of contention. The commission has said UBS may have engaged in misleading and deceptive conduct by representing to PNG that the options used in the collar loan were written at nil-premium.

“That is, nil premium in this context was a clear representation by UBS that it was not separately profiting from the pricing of the option structure over and above its declared fees,” is what the commissioner assisting determined it meant, which was at odds with the work of Brattle.

UBS had, in fact, set the pricing to make money and says it never suggested otherwise.

It claims it did not misrepresent the state through its nil premium claim, and cited contract protocols that this definition applied to a payment due at a certain date. Given all the interest had been paid upfront, the nil premium description was appropriate, UBS said.

On that, the commission said UBS knew that PNG wanted to borrow money at a rate below 5 per cent, so it could be compared favourably with the 5.1 per cent IPIC loan.

The two-year collar loan was represented at a 4.95 per cent rate, but the commission said that since PNG effectively paid at the outset of the loan the implied rate was 5.34 per cent. While that is the case, other terms of the loan may have adjusted.

So UBS has indeed mounted a vigorous and spirited defence against a commission it says has not heard it and relied on flawed evidence.

UBS needs to disclose how much it earned as part of the Oil Search deal.

Time for UBS to come clean on PNG loan

But the commission’s comments show that it is steadfast in its view that the bank left it too late and that its expert is both credible and correct. By failing to produce any witnesses it ceded its opportunity to set the record straight.

Whether this will have implications for UBS beyond a week of bad headlines also remains to be seen.

A new PNG government can’t reverse a deal their formers leaders pursued but have now been told should never have been done, by any bank.

But those very leaders seem to agree that UBS, which itself is under new leadership, should be pursued. That means the consequences of the ill-fated deal will linger uncomfortable in Chifley Tower for a while yet.

The collar loan: The story behind UBS’ ill-fated PNG deal.